Before You Lock Your Money in an FD, Understand How Banks Calculate Your Yield

- The FD Yield Confusion: What's Really Happening?

- Simple vs. Compound Interest: The Basics Everyone Forgets

- Why ‘Simple Interest’ Looks Tempting?

- Where Misleading Practices Can Still Creep In?

- Example

- RBI’s Circular on FD Rates Transparency

- Final Takeaway: Invest wisely

The FD Yield Confusion: What's Really Happening?

In India, no matter how many new financial instruments hit the market, Fixed deposits (FDs) still hold a special place in our hearts.

Why? Because they promise something most other products don't – "Certainty."

When you invest in a Fixed Term Deposit (FD), you already know what you'll get after 3, 5, or 10 years. There's comfort in knowing the safety of capital and the "guaranteed" interest your bank quotes.

But here's the catch.

Every time you want to invest in FDs at any bank, you won't find a single rate. And by human logic, you will end up investing in a bank where the rates look high.

And, reality is that “you will receive no extra amount for this additional percentage.”

Sounds confusing? It is.

Keep reading to learn why banks do this, and whether it affects your actual receivable amount at maturity.

Simple vs. Compound Interest: The Basics Everyone Forgets

See, for any FD you book, the basic school formula always looks for the simple interest rate, and if it's for long term, the compound rate matters.

So, let's assume you put ₹100,000 at 6.6% for 3 years. For the first year, you will receive interest of ₹6,765. This is simple interest.

Likewise, for the 2nd year, your principal (for which interest will be calculated) won't be ₹1 lakh. But ₹106.765. This addition is what we call the power of compounding or compound interest. Now, it can be more than said, due to quarterly compounding.

By the end of the 3rd year, you will finally receive ₹1,21,699 or more. This is natural quarterly compounding, which banks often do.

But here's another twist.

Many banks highlight "higher" returns that look impressive (often shown as quarterly compounded rates) while actually calculating your maturity amount using simple interest. And customers end up investing in banks with higher rates.

Why? Find the answer in the next section.

Why ‘Simple Interest’ Looks Tempting?

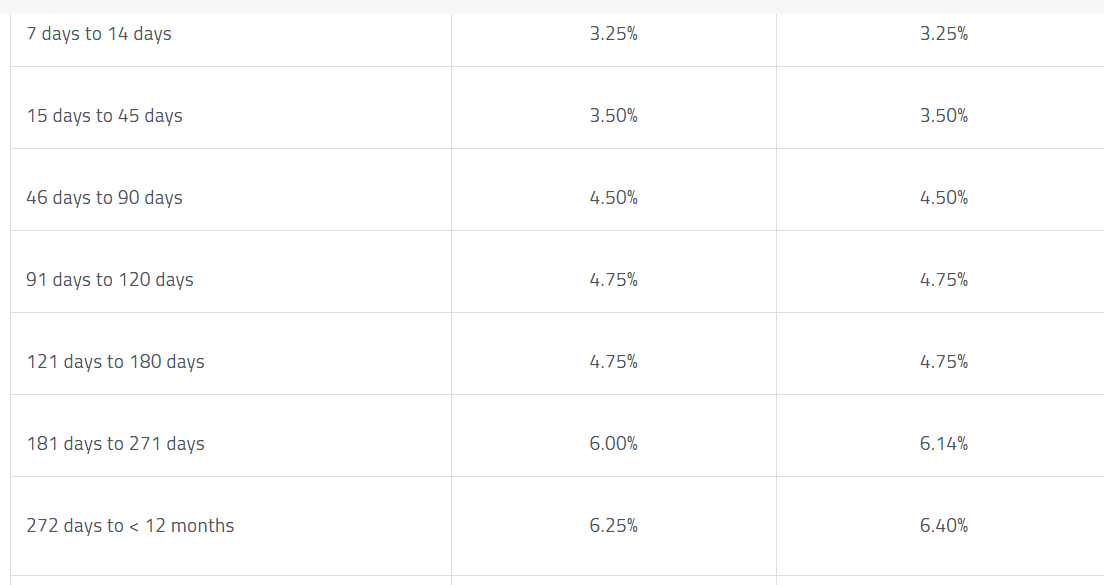

On the majority of bank websites, two rates are shown: "Rate" and "Annualized Rate."

And what's the difference? Simply, the interest rate calculation differs.

In the first column, it's just the FD rate common among the peers. And the second column, usually the "Yield/Annualized Rate," assumes annual compounding and hence, the percent increases after a certain period (as shown below).

Source: Yes Bank

Where Misleading Practices Can Still Creep In?

Every bank will have a different "Annualized Yield", and the method of calculation also varies.

Let's take a situation.

If the bank is following the annual compounding, the interest rate (%) will be less compared to the bank calculating using the simple interest formula.

But why is it high? It's just that the banks don't include interest receipts in the principal. Here, the yield calculation is basically the total interest receivable divided by the tenure (by using the simple interest rate formula).

Hence, the "Annualized Rate" looks attractive. Think of it as a marketing tactic to attract customers.

Surprisingly, in the end, you will receive the exact same amount on maturity. Let's see how!

Example

Assume you're investing ₹1 lakh for 3 years in FDs, the final amount you'll receive is ₹120,650.

Principal = ₹100,000

Tenure = 3 years

By using quarterly compounding,

A = P × (1 + r/400)12

1,20,650 = 1,00,000 × (1 + r/400)12

(1.2065)1/12 = 1 + r/400

1.01565 = 1 + r/400

R = 0.01565 × 400 = 6.26%

Nominal Interest rate is 6.26%.

Annualized Yield (%) calculation:

Interest = Future Value - Principal

= 1,20,650 - 1,00,000

= ₹20,650

Rate (%) = (20,650 / 1,00,000)

= 20.65% / 3

= 6.8%

Now, if you compare the first bank's rate (6.26%), the annualized rate of 2nd bank will look higher (6.8%).

And that's why many customers are reluctant to invest in such banks with higher rates.

However, the reality is that the end amount is the same. Only the bank is gaining new customers.

RBI’s Circular on FD Rates Transparency

Considering this common practice, many banks still use this method as a tool to attract customers. This minor distinction can fool you about the FD yields (despite the same maturity amount).

But the RBI (Reserve Bank of India) circular has something else to state.

As per the Master Directions, banks can show differential interest rates in the following conditions:

The size of the term deposits (also bulk deposits) allows the banks to show differential rates. However, if it's under any government scheme such as the Bank Term Deposit Scheme, 2006, or the Capital Gains Accounts Scheme, 1988, then this rule does not apply.

Commercial banks cannot highlight or advertise only the compounded yield on term deposits without showing the actual simple interest rate offered by the bank.

They must also clearly show the simple annual interest rate, the basic rate you actually earn each year for the same deposit period.

Moreover, the end goal of the RBI is also to ensure that higher-looking figures do not mislead depositors.

Final Takeaway: Invest wisely

After understanding the yield calculation, the truth is, there is a nil difference in the final amount receivable on your FD deposit. But what matters is how the banks might fool you by showing high interest rates.

With that said, it is also important to know that Fixed deposits form a major backbone of the household income. Choosing a bank that offers not just interest rates but also services, withdrawal options, and customer support can help you select a better FD for your investments.

Disclaimer:

The information provided in this article is for educational and informational purposes only. Any financial figures, calculations, or projections shared are solely intended to illustrate concepts and should not be construed as investment advice. All scenarios mentioned are hypothetical and are used only for explanatory purposes. The content is based on information obtained from credible and publicly available sources. We do not guarantee the completeness, accuracy, or reliability of the data presented. Any references to the performance of indices, stocks, or financial products are purely illustrative and do not represent actual or future results. Actual investor experience may vary. Investors are advised to carefully read the scheme/product offering information document before making any decisions. Readers are advised to consult with a certified financial advisor before making any investment decisions. Neither the author nor the publishing entity shall be held responsible for any loss or liability arising from the use of this information.

Related articles: